The big news this week (sort of) has been the rally in the bond market. The 10-year Treasury yield closed on Thursday at 1.3%, which is down 44 bps (34%) from the end of March. That’s a big move in bonds!

So, to recap, the bond market got smacked the first three months of the year, and now it seems to be coming back. What gives?

My guess is that nervous traders and people who sit at home watching financial news are catching up to what we’ve been discussing all year long – inflation is not going run wild (at least not yet) and the Fed isn’t going to be forced to do anything they don’t want to do.

Now that this risk of a return to disco balls and bellbottoms appears to be off the table, bond traders are calming down. This could also be a good thing for stocks. Here’s why…

When yields were rising earlier this year, academics pointed to the fact that a higher 10-year Treasury yield translates to less valuable future cash flows for companies. This is super geeky, but try to stay with me on this one.

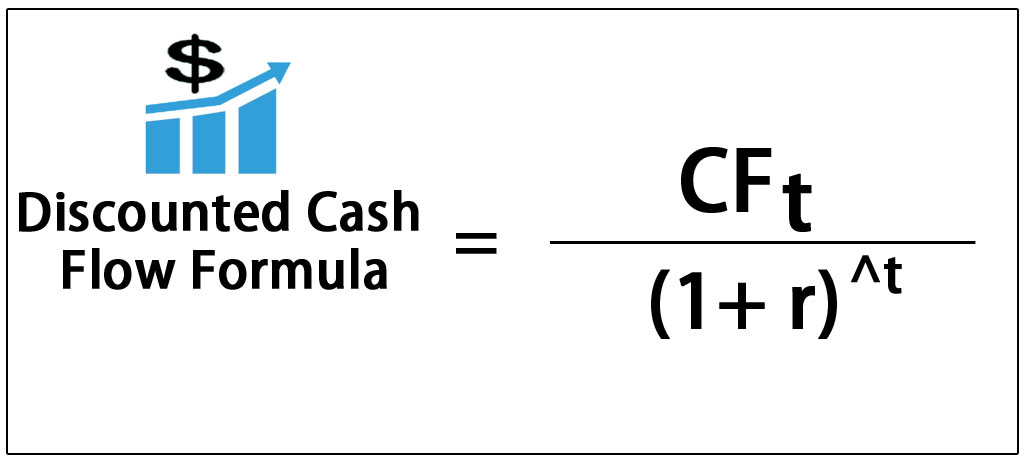

That CFt represents the sum of all future cash flows for a company over some time period (designated by that “t”). Meaning, some junior analyst at a big bank would estimate all of Apple’s cash flows over the next t years and then divide them by r, which is the “discount rate.”

This is a rather nebulous term/idea but think about it as a measure of risk. The higher the discount rate, the less valuable Apple cash flows become because the numerator gets divided by a larger denominator.

Don’t get lost in the math here. Focus purely on the concept – as the discount rate rises, future cash flows become less valuable because the risk to those cash flows has gone up (more risk = less certainty).

Side note.. If you’re wondering what the discount rate for Apple is, then get in line. Nobody knows, and this is one of many reasons why financial theory that’s taught in CFA curriculums and fancy business schools is often so much fun to shred. It’s all abstract. My r for Apple could be wildly different than Tim Cook’s r.

But the 10-year Treasury yield just happens to be the de facto starting point for discount rates. So, even if my r for Apple differs from Cook’s, one thing is likely certain. Both our discount rates start with the 10-year Treasury yield and increase based on our view of the risk to Apple’s future cash flows.

Why does everyone use the 10-year Treasury yield and not some other rate? I really don’t know other than it’s just been that way for a long time.

So, when the 10-year yield rises, all those geeks who run spreadsheets for a living freak out and run into their portfolio managers’ offices screaming that their numbers are coming down. The PMs also freak out and sell stocks down to a level where they want to manage their portfolio’s overall risk.

And when the 10-year yield falls, like it has since March, the opposite should occur. The value of future cash flows rises because the denominator shrinks. The geeks then walk into their bosses’ offices and scream, “I told you!!!” and then PMs buy more.

Again, this is all in theory. Much of professional money management is not this academic, nor do I think that day traders who dip chicken wings in non-vintage champagne after scoring big trades are discounting cash flows of AMC. But this is what pundits will tell you is happening, and while I’m clearly skeptical of just how much it’s used, there is some merit to it.

Another and far simpler reason that falling yields could be good for stocks is that bonds and stocks tend to compete for investor dollars. When bonds become less appealing (like when their yields fall to levels that can’t even beat inflation), stocks usually become more attractive.

Add it all up, and this is what we could be entering over the next few months:

- Earnings season is upon us, and it’s probably going to be strong with a lot of talk about being unable to meet current demand for goods and services (high class problems).

- Bond yields are falling since inflation doesn’t look like it’s going to force the Fed’s hand.

- There still is no alternative to stocks.

I hate predicting short term market movements, but this setup is an interesting one.

I also wonder if falling yields will end this junk rally that we’ve seen since November. I’m not talking all value stocks – just the junky ones with questionable fundamentals. I’ve stressed avoiding this trade all year simply because the timing is nearly impossible (not to mention the potential tax implications). And if this now reverses, it could be brutal for those late to the trade.

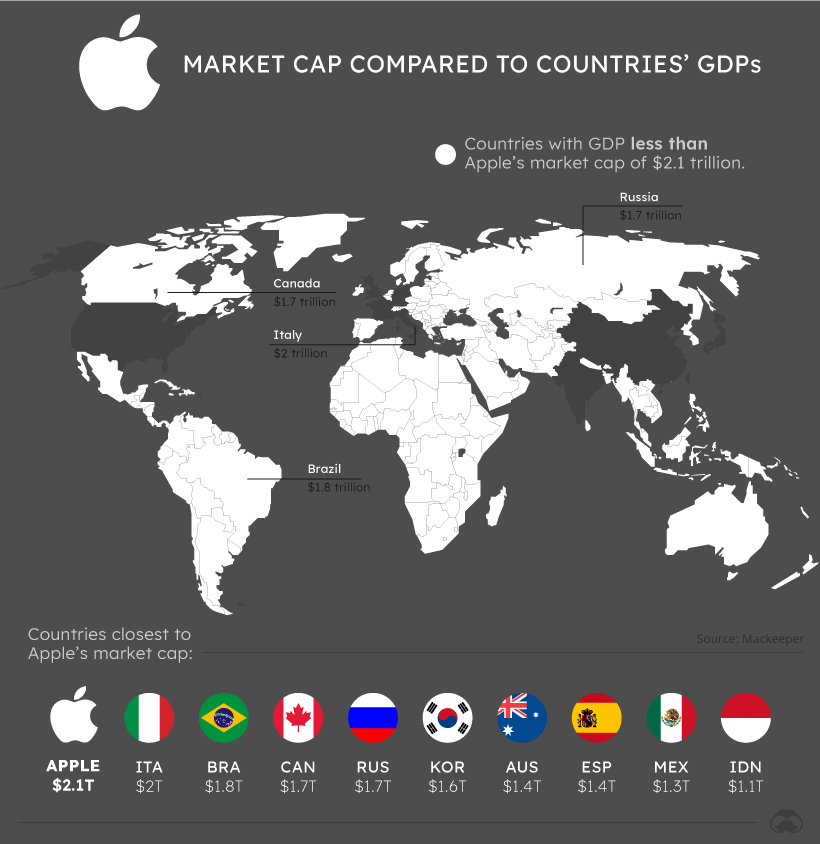

Lastly, speaking of Apple, here’s something that was bound to happen. Big Tech is just too big to not be compared to GDPs of large countries, so here’s a link to just that.

Even though the comparison of market cap to GDP is borderline meaningless, it’s still interesting to see just how big these companies have become. For example, Apple’s market capitalization is larger than 96% of country GDPs. This list includes Italy, Brazil, Canada, and Russia!

Lastly, if you’re bored this weekend or just want to laugh at someone else’s lack of financial literacy, you simply must read this story about how Columbia University and so many other “prestigious” schools are ruining their students’ lives by convincing them they need six-figure degrees to become screenwriters.

It’s a masterful depiction of the most powerful cartel on the planet – the U.S. college accreditation association – and how they’ve been able to use unsuspecting teenagers and twentysomethings as mules to move cash from the government into their coffers for decades.

And since I recently came across a meme generator online, I simply couldn’t help myself. Although this probably isn’t NFT-worthy, here’s my first attempt at a meme (nobody younger that 40 will likely get this one):

Enjoy the weekend…

You must be logged in to post a comment.