Happy Friday!

Quiet week with exception of continued theft, regulatory action, and more tulips budding in crypto land. So, I wrote a primer on how the Fed works and why the upcoming nomination for Fed chair in February is a big deal. Yeah, I know this stuff can be boring, but if anyone other than Powell gets the look, it could impact investment strategy.

Not much else to report other than some quick thoughts on the employment situation. Getting people in good jobs is the single most important factor to a strong economy (and country). We all saw what happened last year when people don’t work. As Blaise Pascal famously once said…

“All of human unhappiness comes from one single thing: not knowing how to remain at rest in a room.”

Well, the data over the past few weeks on employment has been pretty awesome. In fact, here’s a snapshot showing initial unemployment claims is down substantially over the last year.

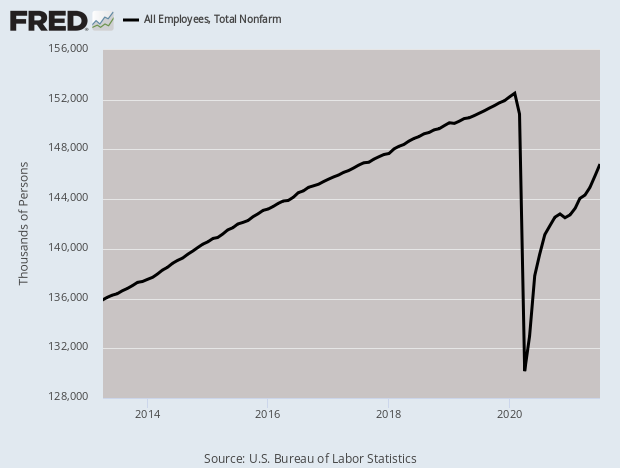

More importantly, here’s where we stand relative to pre-covid. Looks to me that we are maybe 7-8ish million jobs from getting back to where we were (based on the y-axis of the peak minus today). Meaning, we haven’t fully recovered but we are getting closer every day.

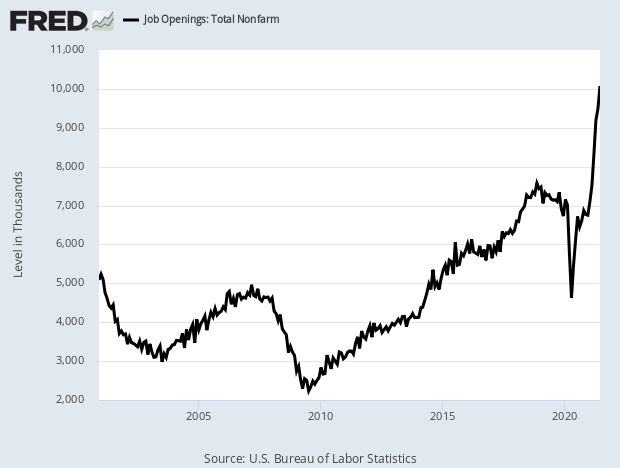

And here’s where it gets interesting… The number of job openings right now appears to be just over 10 million.

Follow the math with me… If we are only 7ish million jobs from getting back to “normal,” and there are over 10 million jobs unfilled right now, then we technically have more job openings than what’s needed to get us back to “normal.”

That’s good!

But what’s less good is that some people are either still getting paid not to work and/or afraid to go back to work. I’m not touching this one, but relatively speaking, this is a high class problem for an economy. Small business owners saying their biggest challenge right now is finding labor and materials is WAY better than post 2008, when their biggest challenge was finding customers. That really sucks.

Now, some may argue that this employment recovery will force the Fed to raise rates faster than expected. I disagree because these are headline numbers. Broad strokes at best, and the Fed has signaled that they want pretty much all subsectors of employment to look strong before they move.

Meaning, they can slice and dice this date a thousand different ways to justify why they aren’t raising rates this year. And since they believe inflation is still transitory, they are covered for quite some time.

Gun to the back of my head and I would guess that tapering begins around year end. They’ll probably start talking about it in their annual meeting in Jackson Hole in a few weeks. But unlike most discussions plagued with academics and economists, they can’t just assume their $120 billion in monthly bond purchases away. They are going to need a plan.

Enjoy the weekend…

You must be logged in to post a comment.