Happy Friday!

This week’s piece is sort of a call to action for clients and advisors. I’ve said for years now that the 60/40 approach was like bringing a knife to a gunfight. So, I wrote a comprehensive note on why I think this to be the case.

Please take the time to carefully read this one and pay particular attention to the last section called “The Bottom Line.” It’s meant to be an analogy for clients to better understand what’s changing in markets these days.

Ok let’s address the market freaking out this week due to Fed minutes, which were released at 2pm ET on Wednesday, that hinted at tapering later this year or early next. Well, that’s an exaggeration because the market didn’t really panic all that much. It fell after the minutes were released, but like every other dip we’ve seen in recent history, it barely lasted.

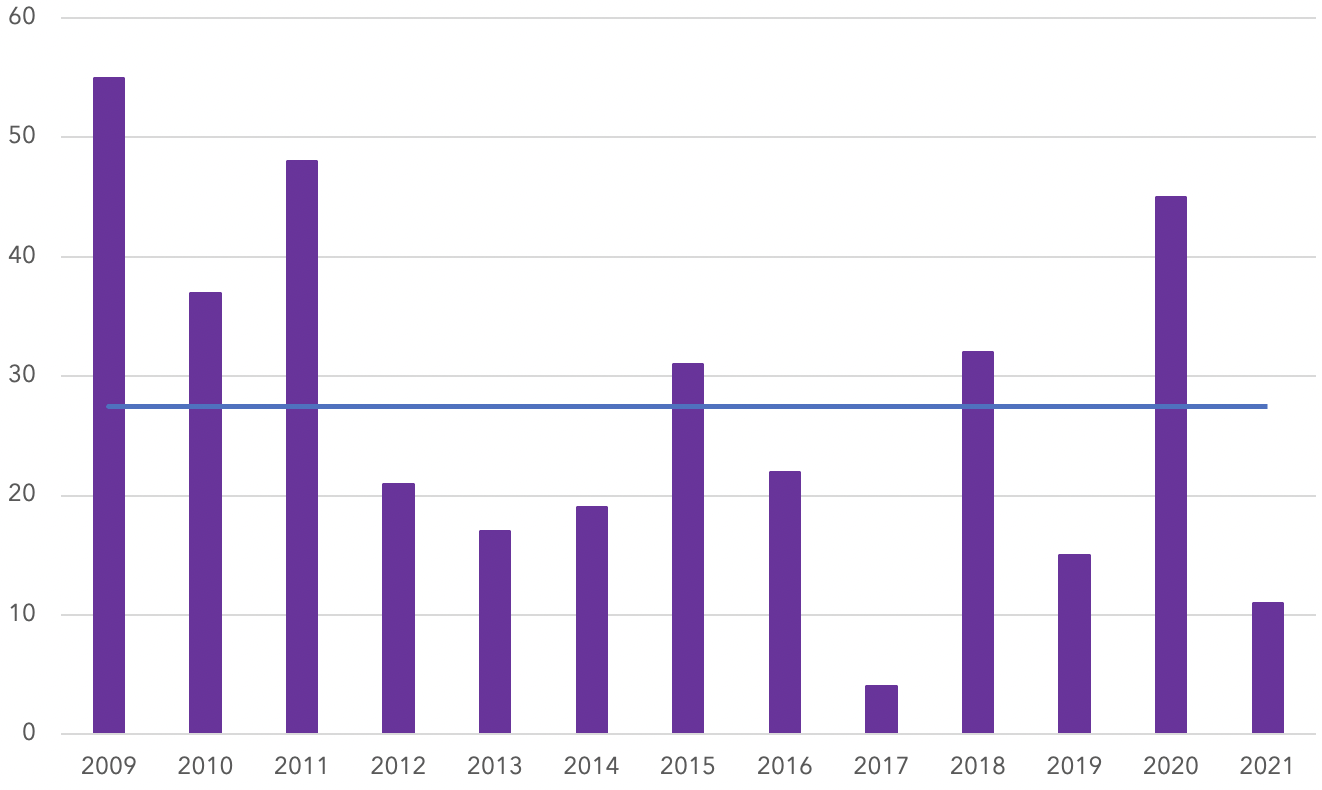

To start, let’s put this “weakness” into context. There’s been very little volatility in the S&P 500 this year. Our team put this table together, and you’ll see that the number of down days greater than 1% in 2021 is trending a lot lower than the average since 2008.

Source: Bloomberg. Darwin Asset Management analysis. As of 8/18/2021

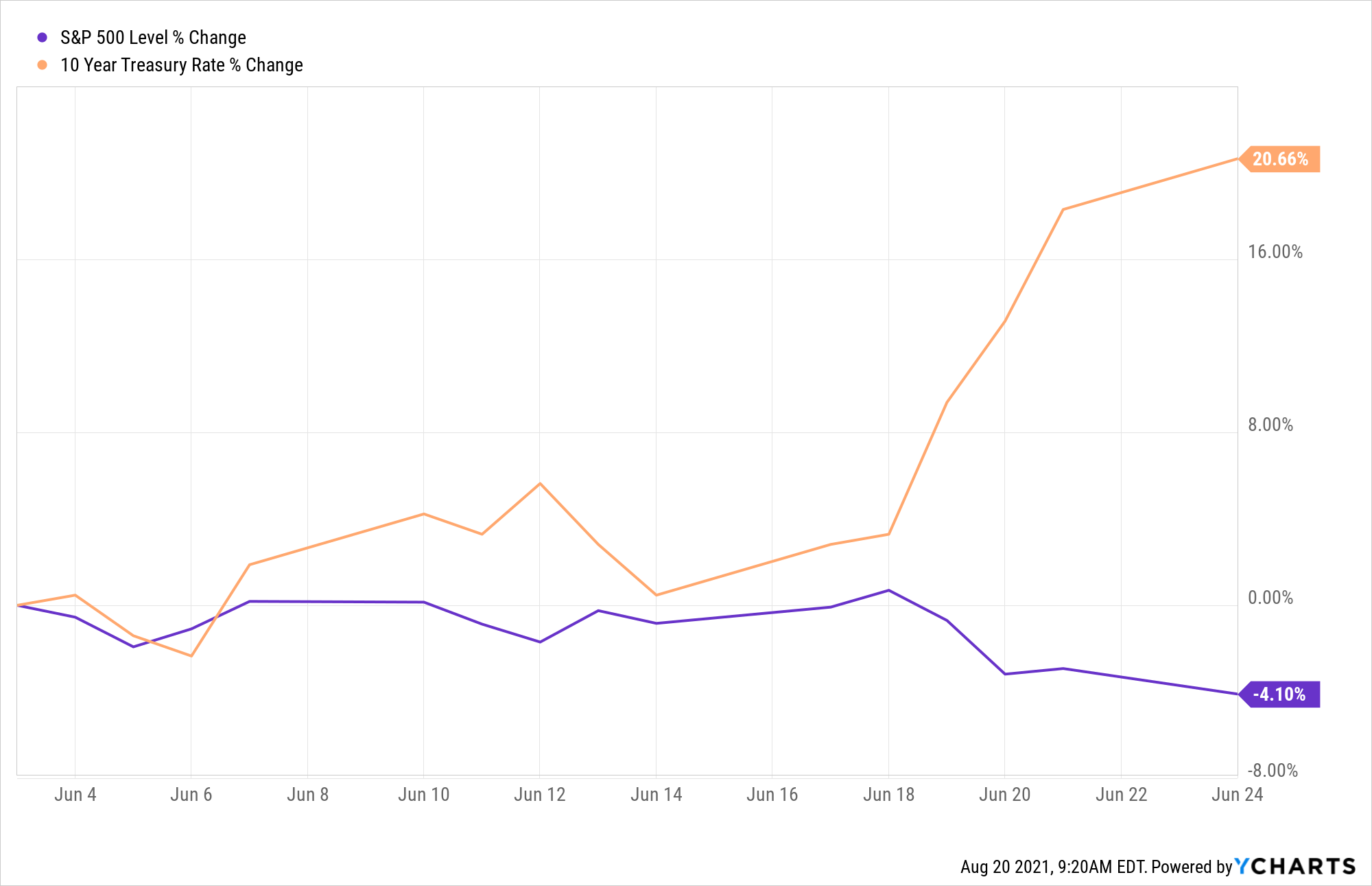

Furthermore, the response this week was nothing compared to what happened when Ben Bernanke ignited the “Taper Tantrum” back in 2013. He caused the stock market to fall over 4% and the 10-year yield to spike over 20% (rising yields = falling bond prices = the bond market was hammered) in a matter of days.

If I were a betting man, I’d wager that the response to tapering in 2021 relative to 2013 will be a non-event for three reasons.

First, the Fed is getting a lot better at communicating to the public. Rewind to the Greenspan days, and his “F off” mentality towards the press and public made every meeting a potential powder keg. Bernanke changed that but hadn’t quite realized how important things like the placement of semicolons can be to people who are betting on the direction of rates.

Today, Powell and team are by far the best communicators (most likely due to leveraging the mistakes of past leadership), and their bedside manner has been pretty effective so far.

Second, last year’s recession was nothing at all like 2008. The COVID recession was what I refer to as a “Plaxico Burress” recession. Things were going great, and then the government shot itself in the foot. It wasn’t a real recession like the one in 2008, which was fueled on excess, over-levered consumers and businesses, and a clueless Fed.

Last year, things were going just fine until people were ordered to stay home. Today, we are recovering about as fast as math allows us to. That’s because none of the excess or issues that fuel recessions existed before COVID, and they aren’t around today either.

This is important because Quantitative Easing is a crutch for an injured economy. The timing of when crutches comes off is crucial, and back in 2013, people were really worried that tapering was happening way too early. Today, not so much. The economic data couldn’t be stronger (relatively speaking), and there are a lot of signs that investors have been preparing for tapering since the Spring.

Said another way, it seems like investors today expect tapering because it makes sense. That wasn’t the case back in 2013. The financial crisis was not only a recession, it was a seriously bad one that was made ten times worse by the regulatory response after the crisis. Hammering the banks like they did made it virtually impossible for the economy to grow. Had it not been for the tech industry and a few other bright spots, we could have easily fallen into another lost decade scenario.

That’s why people freaked out back in 2013. They were worried that the crutches were coming off too soon.

Third, there’s a psychological component to tapering. We fear what we don’t understand, and back in 2008-2013, we knew very very very little about the ramifications of Quantitative Easing. That’s because nobody had ever seen it before. The last time the Fed used it was during the Great Depression, so no investor alive had any context as to how it would play out.

We were sitting on pins and needles for years worried that the egregious manipulation of markets and interest rates by a group of academics and economists who could barely tie their own shoes was going to end badly. But it didn’t. At least not yet.

Fast forward to today, and we’ve seen QE in some form for most of the last 12 years. We are so used to Fed manipulation that it’s become a near permanent fixture to markets these days.

Add all of this up and here’s what I’m telling investors… If you’ve ever had crutches before, you know that those first few days/weeks are wobbly and risk falling down more than once. But over time, your leg heals and gets stronger – something that can only be done by going through the pain and discomfort of removing the crutches.

That’s what will probably happen over the next 18 months. The Fed is going to spend most of 2022 winding down their $120 billion in monthly bond purchases (this is QE), and it’s probably going to cause markets to get a little wobbly at times. But it needs to happen.

Now, the natural response by nervous clients is to just run to cash. Sit on the sidelines, let the Fed finish tapering, and then get back in. If you get hit with this one, I’d respond with the following:

- Cash is trash. Losing money safely for 18 months (or however long it takes) doesn’t sound like a great plan.

- Volatility is NOT risk, and to sell stocks now in the early innings of an economic expansion seems suspect.

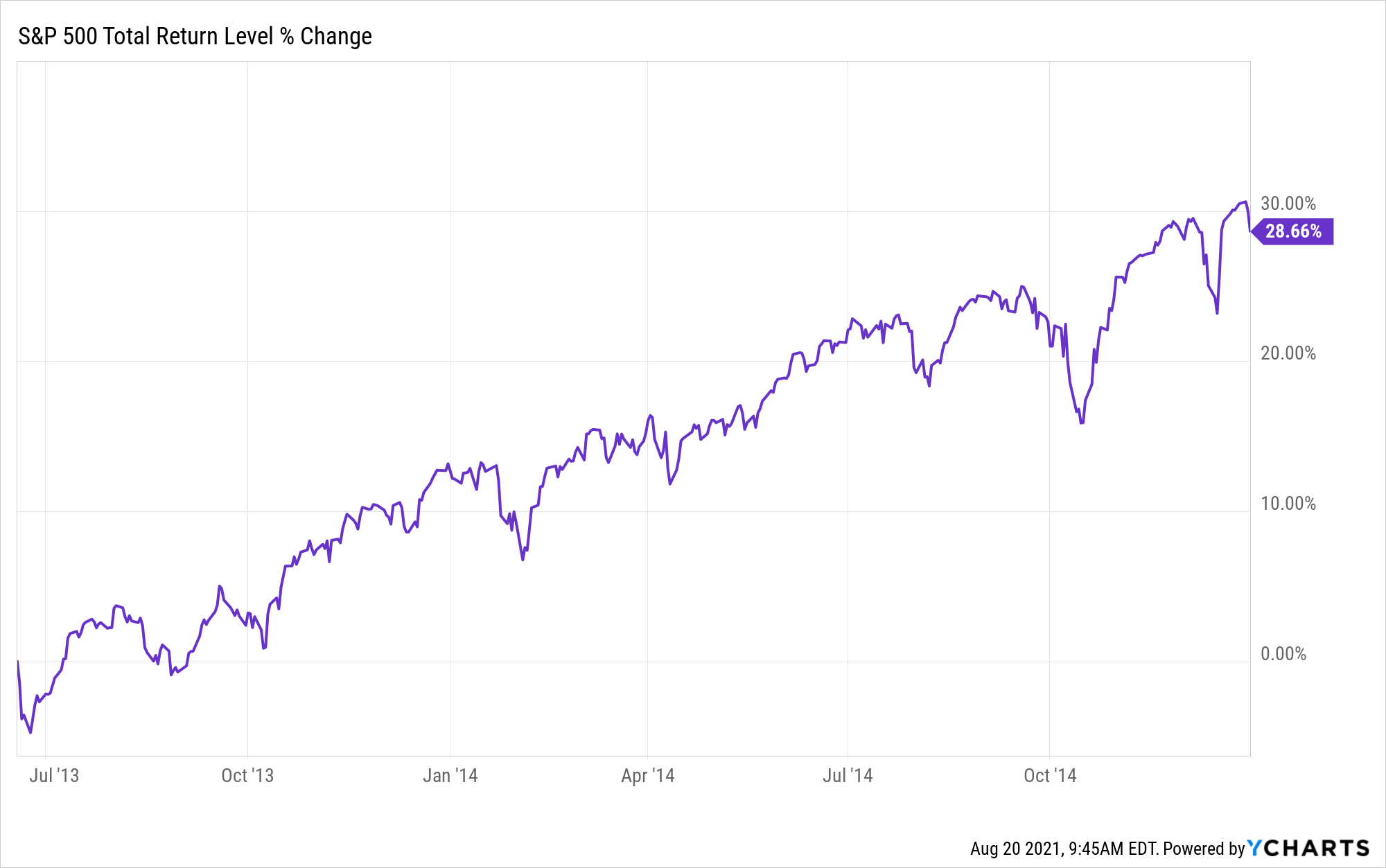

- History would tell you that running to cash may not be the best move. Here’s the S&P 500 from June 18th 2013 (the day before Taper Tantrum) through the end of 2014, which captures the entire period of announcing tapering to completing it. Sitting in cash to avoid volatility would have lost you a near 30% gain in 18 months.

Enjoy the weekend…

You must be logged in to post a comment.