Happy Friday!

I’m hosting a webinar on Monday discussing M&A in RIA-land. I’m going to talk about what you can do to make your practice attractive to an acquirer, how to build enterprise value, and what you should be thinking about if you want to acquire.

This week, I wrote about 20 myths in finance and investing that I like to refer to as “Old Financial Wives’ Tales.” Sort of like, “don’t go outside without a jacket or else you’ll catch a cold,” but for finance.

Ok, let’s get going… I haven’t poked the COVID bear in a few months, so here’s a fun fact from the First Trust COVID Tracker:

“A nationwide study of patients at the U.S. Department of Veterans Affairs from mid-January through the end of June 2021 found that of the total number of COVID-19 hospitalizations, 48% had mild or asymptomatic disease. This has significant implications for the nationwide COVID-19 data dashboards in 2021, and suggests that nearly half of the overall COVID-19 hospitalization numbers represent patients who may have been admitted for another reason entirely or had only a mild form of disease.”

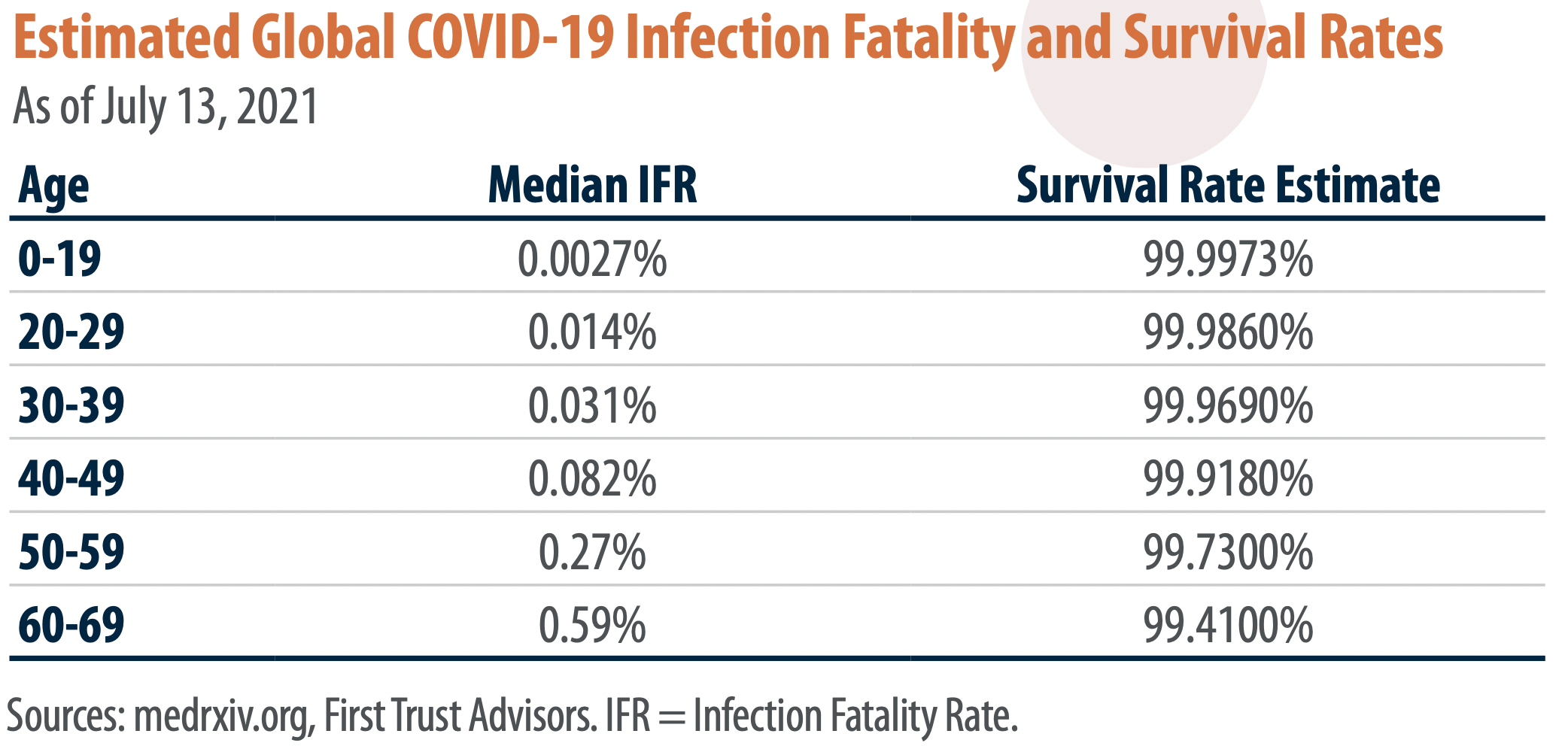

Also, some updated mortality numbers broken down into age ranges:

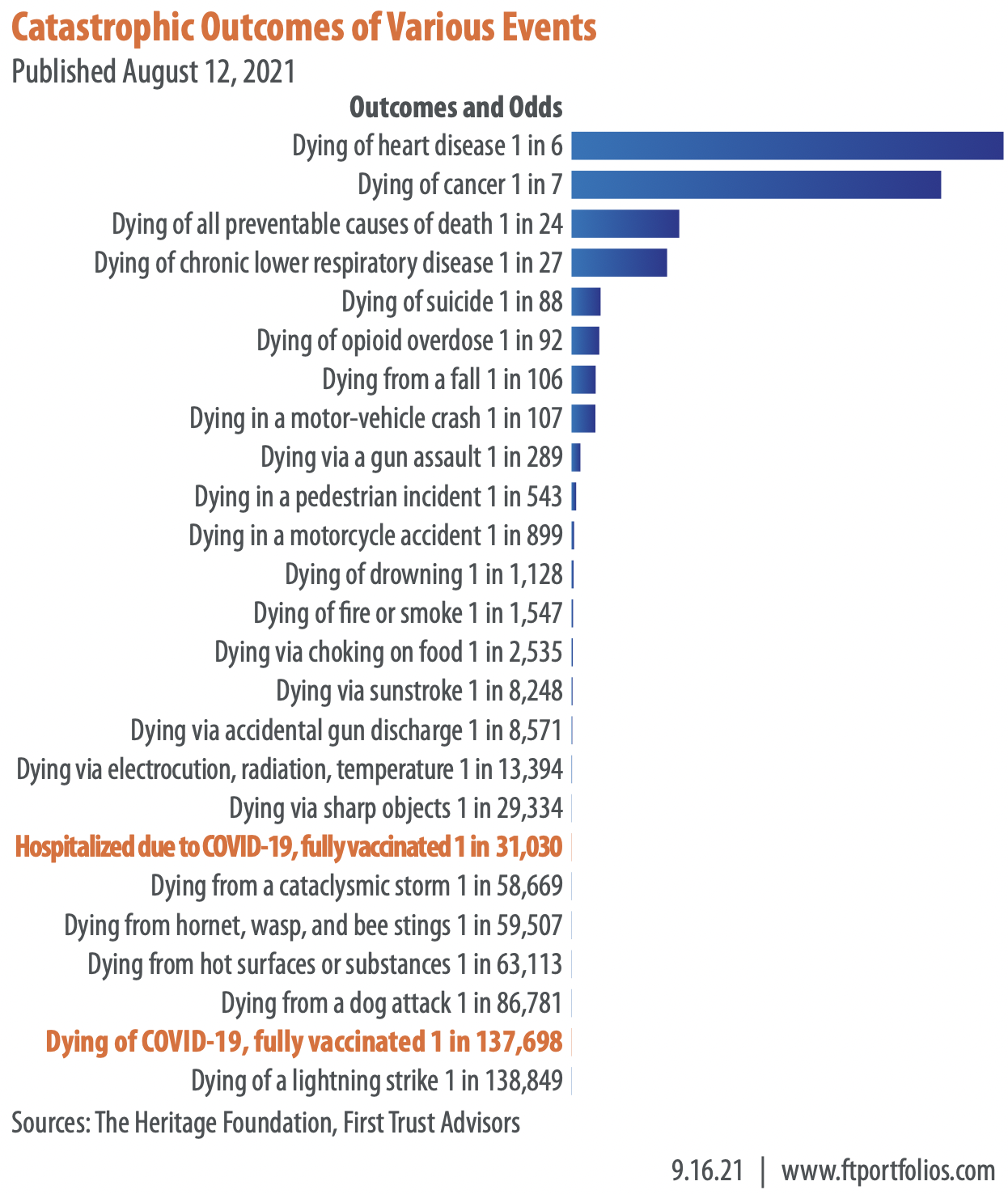

And here’s this:

Now that you’re fired up let’s talk about why we should expect the economy to start slowing down…

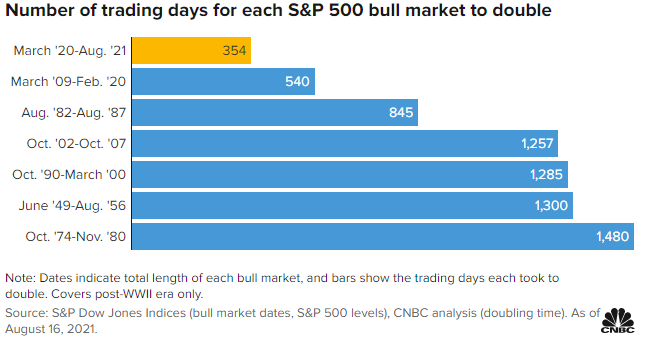

Economic growth has been unprecedented over the last 18 months, but that’s because last year’s recession was artificial. The excesses that typically fuel recessions were not the culprit but rather the government flipping a switch. Hence, this happened…

But as the great philosopher, Axel Rose famously said, “… nothin’ lasts forever, even cold November rain.” I’d wager that we will start seeing growth rates decline by this November.

To be clear, I’m talking about the second derivative (a fancy way of saying “rate of change” or, better yet, “decelerating”). That means the economy should continue to grow unless DC screws up again and shuts everything down, but at a slower pace.

For example, Brian Wesbury said this in his blog earlier in the week (emphasis added by me):

“The key problem for real GDP is that the massive and unsustainable fiscal stimulus and income support that happened during COVID pushed retail sales well above the pre-COVID trend. Retail sales in July were 17.5% above the level in February 2020. To put that in perspective, in the seventeen months before COVID, retail sales were up 5.1%. There is only one way retail sales can grow 3x its normal rate while millions are unemployed and the economy was locked down – the government pulled out the credit card.”

Consumer spending and retail sales are 70% and 30% of gross domestic product (GDP), respectively. If these start to materially slow now that the government is putting away that credit card, then it’s hard to imagine how the rest of the economy can pick up the slack.

To be even more clear, there’s no reason at all to fear slower growth rates. This is how math and physics work. I’ll take slow and steady growth any day over what we’ve experienced this year because it’s more sustainable. But this normalization could lead to some volatility and other bumps.

To be even more abundantly clear, I’m not implying a shift from bullish to bearish. No alarm bells are sounding. All I’m saying is that the last year has been magical for stocks, and some of that pixie dust could start to go away (slower GDP growth = slower corporate profit growth = less fuel for stocks).

Luckily, there’s still more than enough fuel for stocks. One source, in particular, is something we’ve discussed ad nauseum – there’s nowhere else to go.

For a long time, the 60/40 portfolio (60% in stock and 40% in bonds) was pretty much all you needed to diversify because bonds offered attractive yields when the economy was headed into a recession. This “substitution effect” is why we often saw a negative correlation between stocks and bonds.

Today, this opportunity for diversification isn’t the same because the real yield on the 10-year Treasury bond (the de facto benchmark for interest rates) is negative. Meaning, take the current 10-year Treasury yield at 1.36% and then subtract inflation from this, and you get a negative number (this is the “real” yield).

This makes the 60/40 playbook, or any portfolio dependent upon bonds, challenging to manage because it’s not as simple as assuming that 40% will be there to smooth out the ride when things get weird.

This is why we changed our approach to fixed income back in May 2020. We got more active, granular, and unconstrained in trying to navigate this crazy world and prepare for what could come.

Anyway, here’s a stellar excerpt from Eddy Elfenbein’s blog post earlier this week that touches on this very subject (note that “TIPs” refers to the real yield of the 10-year Treasury bond (what we just discussed above)):

“… if you take all the days collectively when the 10-year TIPs has yielded 1.67% or higher, then you see that the stock market had a negative return. Stocks were a net money loser.

But when the TIPs yield has been 0.00% or lower, then the stock market has delivered an average return of more than 38% per year. This makes sense, but seeing the numbers is still surprising.

In short, the higher the TIPs yield, the worse it is for stocks. The lower the TIPs yield, the better it is for stocks. Nothing more complicated than that.

The TIPS tipping point seems to be at 0.5%. Anytime the yield on the 10-year TIPs is 0.5% or greater, then the stock market has delivered an annualized return of 5.1%. That’s probably less than the return of the TIPs bonds. But when the 10-year TIPs yield is under 0.5%, then the stock market has delivered an annualized return of 23.3%.

As I said before, the current yield on the 10-year TIPs is -1.05%. That isn’t just low – it’s close to as low as it’s ever been. The 10-year TIPs yield hasn’t been positive in 18 months. For now, the bond market is signaling more good news for stocks.”

Add it all up, and even though growth may be slowing down over the coming months, There Is No Alternative (TINA) to stocks, which is unlikely to change anytime soon.

Enjoy the weekend…

You must be logged in to post a comment.