Happy Friday!

We are launching a robo solution in April, so I wrote about robo-advisors this week in the context of technological progression. Financial services did a good job fending off technology for as long as they did. Still, with VC-supported fintech and inefficiencies that were just begging to be annihilated, this industry is now in tech’s crosshairs.

Robos have been around for a while, but I still think they are misunderstood by both advisors and investors. As in…

- Robos are only a threat to those advisors who view them to be a threat, and

- Investors who view them as a cheaper alternative to traditional advisors are swapping an apple for an orange.

We are using our robo to disaggregate the advisory offering to target prospects who don’t need the whole shebang. Then combine our award-winning commentary, endless sarcasm, and support, and now you have something special. At least, I think so. Time will tell…

Get ready

I’m going to try to get in front of this story. The yield curve is flattening and could invert. I’m not dumb enough to make that call that it will, but we’ve seen portions of the yield curve already inverted (3yr-10yr in particular). The spread to follow is the 2yr-10yr, and it has flattened but not inverted.

While some believe this is a precursor to a recession, I view it more as a precursor to poorly-written Wall Street research and the media running stories about an impending recession. As Paul Samuelson once said, “Wall Street has predicted 9 out of the last 5 recessions,” so let’s see why.

Yes, the yield curve matters. Banks typically can’t make money when long-term yields are lower than short-term yields because they borrow short-term and loan out long-term. That spread is their margin, and banks don’t make money when it goes away.

Since spending is 88% of our economy, banks are critical because they are the gatekeepers to capital. If banks don’t want to lend, like after the financial crisis, the economy struggles to grow because it’s hard to buy cars and houses without access to capital.

But as we discussed a few weeks ago, there are a lot of factors that drive long-term rates. That’s why an inversion this time (if it happens) should not be viewed as any line in the sand.

Anyway, I’m going to tackle this subject over the coming weeks, so more to come. For now, just know that…

- The yield curve is important and worth watching. When it inverts, it’s a sign to do more research rather than panic.

- It is NOT a trigger switch. It has to stay inverted for a while to have any impact.

- Even if the next inversion leads to a recession, inversions precede recessions by 2 years on average.

Huh?

The SEC now wants to regulate climate. I’m serious. Here are the 510 pages of new regulation that was voted into action this week. But I know you won’t read that, so here’s a summarization courtesy of the Wall Street Journal.

You may be wondering why the SEC is regulating stuff like this because I’m wondering why the SEC is regulating things like this. I get that ESG investing is hot right now, and the large index funds are highly political, but this one is a head-scratcher.

Let’s push aside the reality that ESG investing is highly flawed in its current format. Canceling stocks like celebs on Twitter does nothing to support whatever cause is being supported. Period.

The irony is that ESG funds should be doing the exact opposite – buying up lots of stock and/or waging proxy battles like Engine No. 1 did to Exxon. That gets you in the board room, where real change can happen.

Maybe this has to do with Biden being unable to get climate initiatives through Congress? Or maybe ESG funds realize their current strategy of not buying stocks isn’t going to work, so now they’re lobbying the SEC? I don’t know, but I’m sure this will probably end up in the courts, so stay tuned.

A bad day in bonds…

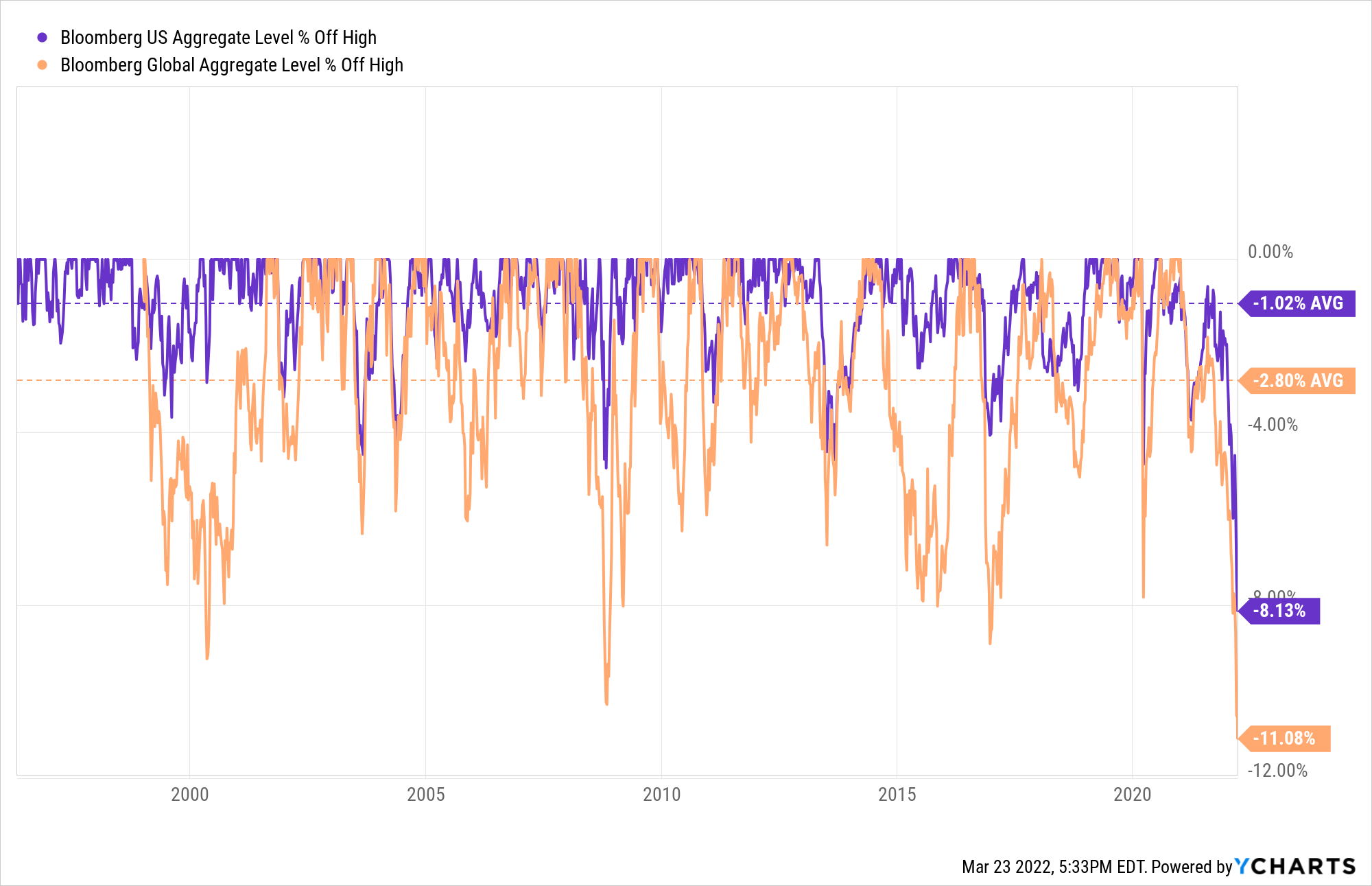

There’s an old saying that a bad year in bonds is a bad day in stocks. That’s been the credo for diversifiers who defend bond allocations. The diversification over time will pay off etc., etc. Well, check out this drawdown chart from Wednesday…

Wow! This is the worst drawdown for the Global Agg ever (data going back to 1990). It’s the worst drawdown in the U.S. since the Volker era (the early 1980s).

I loathe the term “bloodbath,” but if this isn’t a bloodbath for bonds, then I don’t want to know what is. Everyone is so focused on the equity market this year. Still, this chart is all the evidence needed to see why the past months have been challenging for anyone who’s not massively overweight energy.

Holding back vomit

If you’re looking for something to ruin your weekend, read this. A colleague sent me this a few days ago, and I knew I shouldn’t have read it, but I did anyway, and now I hate my life.

Enjoy the weekend…

You must be logged in to post a comment.