Happy Friday!

This week I wrote about this drawdown relative to history, why there’s nowhere to hide, and what investors should do now that we’re deep into a bear market. No investor wants to hear those three dreaded words from their advisor, but within the proper context, they can still be powerful enough to keep clients on track to meet their goals.

Lot of stuff to discuss this week, so let’s dive in…

There’s a leaky faucet at the FOMC

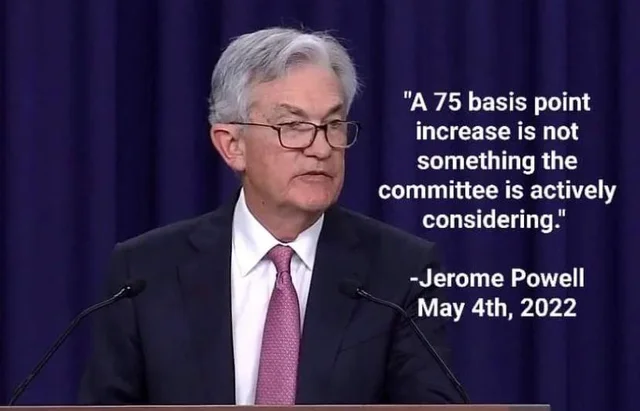

Here’s a rule of thumb for financial news. When the Wall Street Journal reports on an unexpected move by the Fed two days before an FOMC meeting, the odds of it being accurate are right around 98%.

It’s not because the WSJ has some crystal ball but rather very well-placed sources that strategically leak information to them. Monday was a perfect example of such a leak, as the world learned that the Fed was planning to raise their target rate by 75 bps instead of 50 bps.

The aftermath of this article, combined with the inflation report last Friday, was savage on markets. At one point, investment-grade corporate bonds were down 2.3%. That doesn’t happen often.

But like I said, there’s zero chance this leak came as a surprise to the FOMC. The Fed 100% wanted this to be priced into markets before Wednesday’s meeting.

Maybe it’s because we are headed into a 3-day weekend, and J-Pow wanted to give markets a few extra days to digest this move. You know, because he said the following just six weeks ago:

My view remains unchanged here. Raising their target interest rate is fine if the Fed wants to get inflation under control, but inflation is just as much tied to the money supply. They’ve already begun quantitative tightening to the tune of $47.5 billion/month and plan to double this amount in September. The problem is that their balance sheet is $8.5 trillion, so any material impact could take a while.

But to be completely honest, I’m torn here. On the one hand, I want inflation to moderate asap. I’m tired of these prices at the pump, just like everyone else. But on the other hand, I love the inflation memes. I really don’t want memes like this or this to go away (turn on your sound, or else it won’t be as funny). Or these…

It doesn’t matter your political, educational, or spiritual upbringing. These are objectively funny, and if the Fed gets its way, then what? Will we be relegated to only memes that shred all these brain donors that lost their life savings to death-spiraled algorithmic stablecoins?

Don’t misunderstand; those are funny too. But I’m a big believer in diversification, so I’d like to see inflation moderate from here. I just don’t want it to go so low that sourcing future memes becomes more time-consuming.

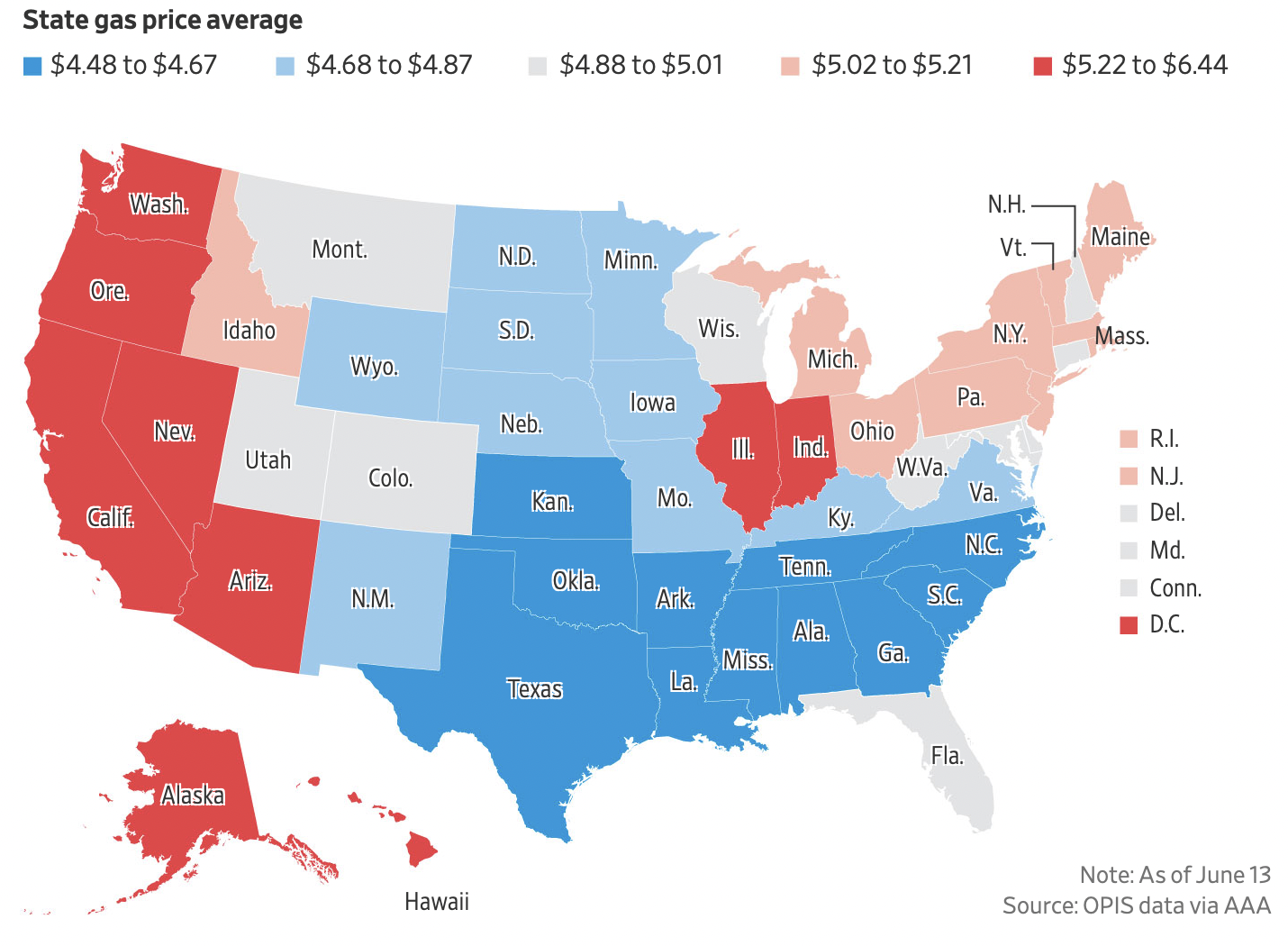

Speaking of gas prices

Here’s a cool chart from the WSJ comparing gas prices across the country. I was in the People’s Republic of California last week, and damn. Seeing $8.00 in San Francisco was not as funny as I expected. I almost, almost felt bad for all those zipped hoodies. Almost.

Speaking of brain donors

Harry Markopolos was the guy who took down Bernie Madoff, and the story goes that it only took him 5 minutes to realize that Madoff was a scam. He apparently dug into the numbers and discovered that Madoff’s returns went up at a 45-degree angle every year with no variation. The problem is that 45-degree angles don’t exist in finance.

Want to know what else doesn’t exist in finance? Large expected returns with little to no risk. But for some reason, this is a concept that millions of people either can’t accept or simply forget.

We can’t go a week without some crypto network and/or coin blowing up, and the Celsius network is the latest to grab headlines. I’ll spare you the boring details, but the lesson learned from Celsius, Terra/Luna, and every other clown show in crypto that offers 18% yields when the risk-free rate is 0% is tremendous risk is involved.

It doesn’t work any other way. These websites and marketing materials can put as much lipstick on a pig as they like, but nothing can alter financial DNA. That’s why when I read stories about people who lost their life savings, because they reached for yield, they appeal to emotions that I just don’t have.

Maybe the recent push by some states to require financial education will help, but I’m skeptical. Human behavior hasn’t changed all that much over the last several centuries, so we’ll just have to wait and see.

OMG!!!

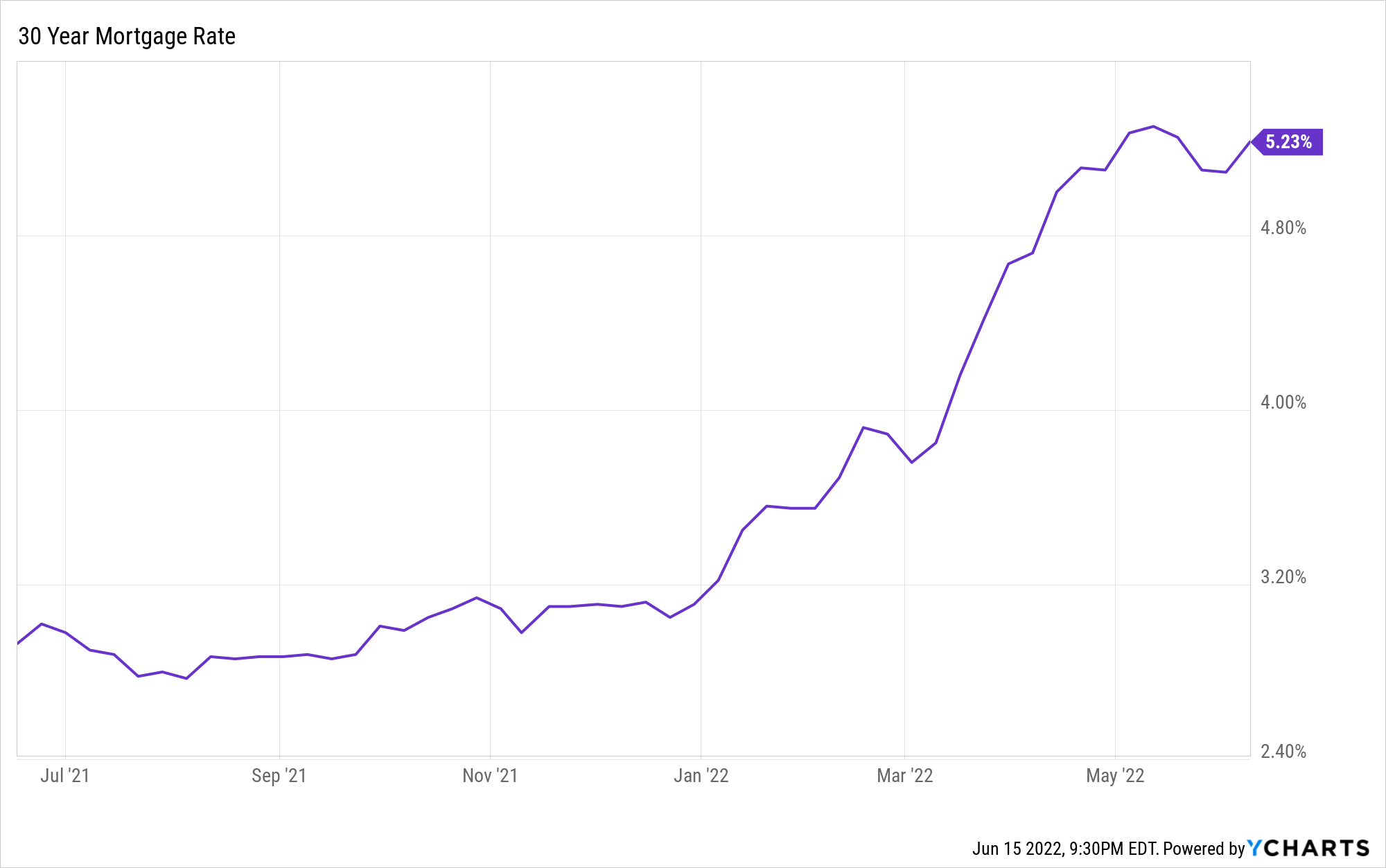

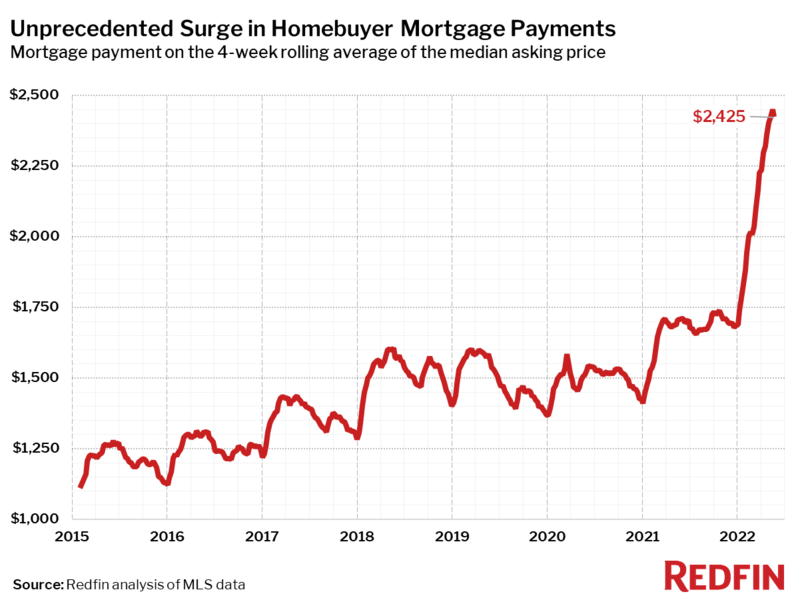

On Tuesday, the 30-year mortgage rate shot up to 6.28%. For scale, it was 5.5% a week ago. There hasn’t been a move like that since the taper tantrum back in July 2013. In fact, the chart below shows that the 30-year mortgage has shot up 63% since January. Wow!!!

The chart below gives a visual of how big of a deal this could be to consumers who are now shopping for a mortgage.

Now, let’s be sure we don’t overreact here, either. This increased payment mainly impacts current shoppers who need a mortgage and anyone in a variable mortgage that hasn’t reached its cap. Oh, and those mortgage brokers getting laid off as we speak. I’d wager that this isn’t a huge subset of consumers.

We may see a more direct impact on the psychology of existing homeowners if the broader housing market comes to a halt. If it did, maybe some will postpone renovations, or perhaps a drop in home equity makes them think twice about that vacation. Also, those who are dealing with rent inflation who can’t buy. Hard to say right now, but this is what I’d be more concerned about down the road since 70% of the economy is consumer spending.

But like I’ve said 100 times over the last year… The housing market could not be more different than in 2008, so I don’t see this as an impending crash like in NFTs, crypto, and sneakers. There’s still a supply problem, and it’s been around for 12 years. I don’t see how rising mortgage rates will solve this anytime soon.

If you’re not part of the solution…

Roughly twelve minutes after receiving my undergraduate diploma, I arrived at the scary conclusion that I had nothing tangible to provide the world. Sure, I had completed four years of engineering curriculum, but all that taught me was that I longed for something more by giving less.

After a few weeks of wandering aimlessly, I was introduced to a profession where “doing the least amount possible to get by but still looking good” was the norm, and missing deadlines and avoiding deliverables was rewarded.

This opportunity sounded too good to be true. Even the name was sexy… “Management Consulting.” The opaqueness and lack of specificity convinced me I had found my calling.

I eventually spent the first decade of my career as a consultant, and I loved every minute of it. When friends and family asked me what I did for a living, I simply replied that I was a “consultant.” The look on their faces was always the same – a cocktail of immediate recognition of the job title mixed with not knowing what it meant.

Anyway, I read an article in the Wall Street Journal this week that chronicled a wild trend in top business schools. Top management consulting firms are apparently giving offers to graduates before they even start their MBA program.

While this may sound ludicrous to those who have jobs that actually matter, for those current and former consultants out there, it makes total sense because we know the real reason why consulting firms exist in the first place. It’s arguably the most straightforward business model out there, and it goes something like this…

Most CEOs at large firms that can afford a tier-one consulting firm got in those seats by (1) making tough decisions when they mattered most and (2) knowing exactly who to throw under the bus when those decisions failed. Consulting firms scratch this itch perfectly.

If their recommendations result in a favorable outcome, the CEO and/or executive team takes all the credit. This generates massive “career yield” because they’ll be rewarded with big bonuses and promotions (numerator) for spending shareholders’ money and doing zero work (denominator).

If their recommendations do not result in a favorable outcome, the client can go to the board and say, “Hey, look… I hired a bunch of really smart consultants with fancy MBAs, and they told me this was the best option, etc., etc., etc.”

Simply put, being able to take credit for good stuff while avoiding any consequence for bad stuff is incredibly valuable and always in demand in corporate America. That’s why consulting is such a high-margin business.

But as these budding MBAs are soon to learn, high-margin businesses attract competition. That’s why there’s a handful of these tier-one consulting firms, and they all compete to get the best and brightest talent.

To be clear, it’s not because these MBAs produce the best ideas for clients. It’s just so that managing partners can pitch prospective clients that his/her team has the most elite MBAs. The firm with the most MBAs will probably win the most business because size matters in deals like these.

The bottom line is that if you’re not part of the solution, there’s good money to be made in prolonging the problem. Extending job offers to soon-to-be $250k debt-laden grads that could have replicated their education with a library card and a refresher of third-grade math makes complete sense because these consulting firms will make a killing prolonging the problems facing their clients.

God I love capitalism. Enjoy the weekend…

You must be logged in to post a comment.