Happy Friday!

The year’s first half was the worst for the S&P 500 going back to 1970. It peaked on the first trading day of the year, lost over 13% in 107 trading days (correction phase), and then another 12% in 7 days (panic phase). The mild recovery since then puts it around a loss of 20.6%.

Get ready for an onslaught of punditry from the talking heads. Advisory clients will have nowhere to hide, so remain proactive on communication by sending out stuff like this weekly (reach out if you need a copy). It dives into what’s been driving the bear market and how good advisors deal with them through robust financial planning.

And as we celebrate the 4th on Monday, we all have clients who think our country is headed to the brink of disaster – high inflation, political mishaps, social media, government debt, etc.

We may have problems, but try living in any other country for longer than 72 hours. There’s a reason why 95% of entrepreneurship and innovation in this world are born here and will continue to be for the foreseeable future. Go USA…

Are we close to a bottom?

Equity markets usually bottom before recessions begin, and they are already rising by the time the recession is underway. This happens because stocks anticipate 6-9 months in the future (I have no idea where the 6-9 months comes from or how this is measured, but everyone on the sell side says so, so it has to be true).

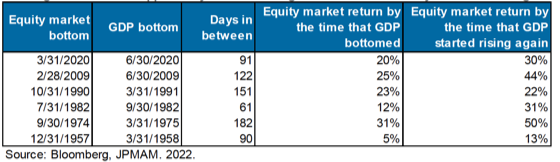

Check out this table from Michael Cembalest at J.P. Morgan. His point is that there’s an opportunity cost of waiting for the economic recovery before investing.

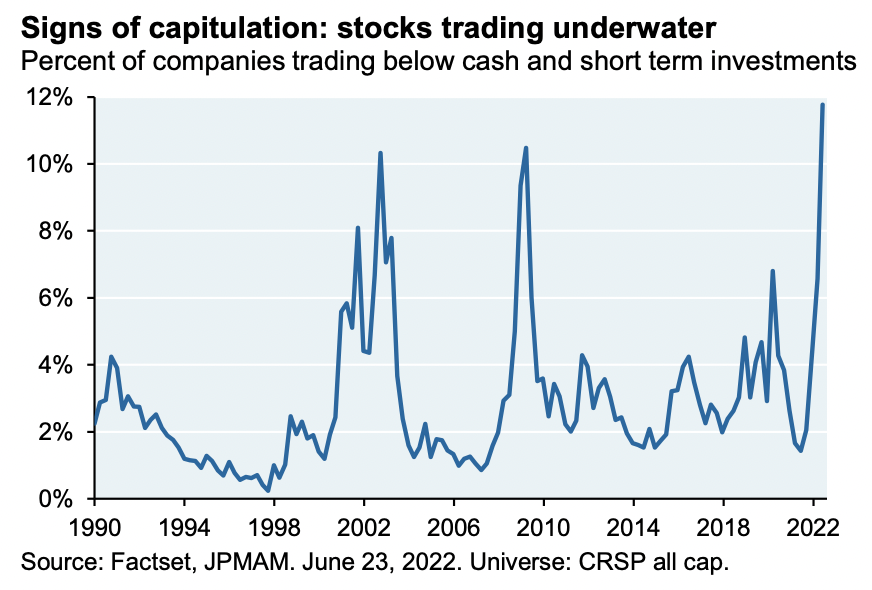

Tangentially, here’s a stellar chart that suggests we could be close to a bottom in stocks:

In layman’s, this chart measures investor capitulation – how many investors have thrown in the towel measured by the percent of companies trading below the cash value on their balance sheets.

Here’s another way to think about this concept. If Elon Musk were to buy any of these companies, he would pay less than the total value of the cash sitting in that company’s bank account plus whatever that company has in T-bills, etc. This makes zero sense, and the fact that it’s at a three-decade high is absurd.

To be clear, insolvent companies can trade below cash value, but that doesn’t happen all that often. So, to say that 12% of companies right now are insolvent? No shot.

I’m not a market timer, but if there’s ever been a sign to make a tactical move, this seems like a pretty good one. Capitulation is higher today than in the depths of the financial crisis? Come on.

Follow the money

I order Starbucks when I travel because the lack of depth and structure combined with its Adderall-style caffeine level provides a welcoming consistency when away from home.

Last week, I ordered a small iced coffee at a Starbucks in Tampa, and here’s an excerpt of the conversation that ensued upon receiving my order:

Starbucks guy: “That will be $4.03… Sorry”

Me: “Huh? Why are you sorry?”

Starbucks guy: “$4 for a small coffee. I keep wondering when people will stop paying.”

Me (upon realizing that I just paid $4 for ice and like 3 ounces of coffee): “Yeah me too.”

I’m very curious about when we’ll hit widespread demand destruction. So much that I gave this guy my email address to let me know when he sees customers pushing back (don’t worry, I gave him my burner email just in case he turns out to be a psycho).

I’ve always felt that the best calls you can make as an investor don’t come from databases but from observation and talking to people on the front lines. Because by the time stuff like this shows up in official data, it’s already too late.

He said what?

Jerome Powell said the following during an interview this week:

“I think we now understand better how little we understand about inflation,” Powell said.

“That sounds very reassuring,” Lacqua responded.

“No, honestly, this was unpredictable,” Powell replied.

Clearly, the only subject the Fed knows less about inflation is humor. I’ve been writing about inflation since June 2020, and I’m nowhere close to being smart enough to work at the Fed. Want to know how so many saw this coming?

It wasn’t by using a Drogan’s Decoder Wheel from a box of Lucky Charms. All we did was take those pesky econ 101 lessons and apply it to the money supply. When the supply of something spikes and demand remains relatively constant, the value of that good falls. This is gravity in economics.

The government increased the money supply by over 40% before the lockdowns. How, how, how, how, how, how did the people who increased the supply not see the supply increase coming?

Some say the CDC has lost all credibility, and others say the Supreme Court has. I’m not touching either of those, but where it’s indisputable is with the Fed.

Anyway, let’s shift focus back to the money supply because some good news came out this week. The money supply has finally fallen to the slowest growth rate since 2019.

To be clear, it’s not shrinking and probably won’t because those stimulus checks now belong to consumers (property rights prohibit the government from taking it all back). But inflation probably isn’t going back to pre-lockdown levels until the money supply moderates.

Speaking of inflation…

Gavin Newsom is the divine leader of the People’s Republic of California, and this week he announced that Californians under specific income thresholds will be receiving “inflation relief checks.”

This is stellar. Let’s provide temporary relief from inflation by doing more of what caused inflation in the first place. Normally, this would be the point where I say something like, “this could only happen in California,” but I’d wager that New York and others will follow the closer we get to November.

It’s not just me!

This is a great article for anyone who can’t understand why conservative and moderate allocations this year haven’t looked conservative and moderate. I’ve been saying this for months, but much like my kids, having a third party reiterate is often needed before concepts sink in.

Enjoy the weekend…

You must be logged in to post a comment.