Happy Friday!

This week I wrote about the recent strength of the dollar and why the media views every move of the dollar negatively. If it weakens, it’s one step away from hyperinflation, and when it gets stronger, the story becomes weaker earnings for multi-national corporations and “doom loops.”

The TLDR version is this… We are Americans. Our entitlement mindset spans beyond ignoring issues relevant to the rest of the world, like exchange rates.

Since our paychecks, bills, and investment returns are denominated in the same currency that drives global trade, we can pretty much dismiss these stories. So yeah, ignorance is bliss.

As always, if you want a copy, just let me know…

Bad news is good news

I feel like we’re at the point in the cycle where any news indicating the economy is slowing down on its own is good for financial markets. That’s because it shows the Fed that their policy decisions are working, so they won’t feel as much pressure to keep hiking rates.

If so, we should expect to see most economic news that points to a slowing economy support asset prices (or at least not knock them down any further). I’ve seen some instances of this already, so be on the lookout for more.

As we’ve recently discussed, the equity market tends to bottom several months before the economy does, so there’s a potential cost to clients who interpret this negativity as a sign to run to cash. This will become more challenging in the coming months as the negative news flow likely increases.

Said another way, if you think it was hard to time an exit and re-entry six months ago, it’s likely WAY harder today. Since we are presumably getting closer to a market and economic bottom, the margin for error has shrunk big time.

I, for one, had no interest in playing the timing game back then, and I sure don’t want to start now.

Talking their own books?

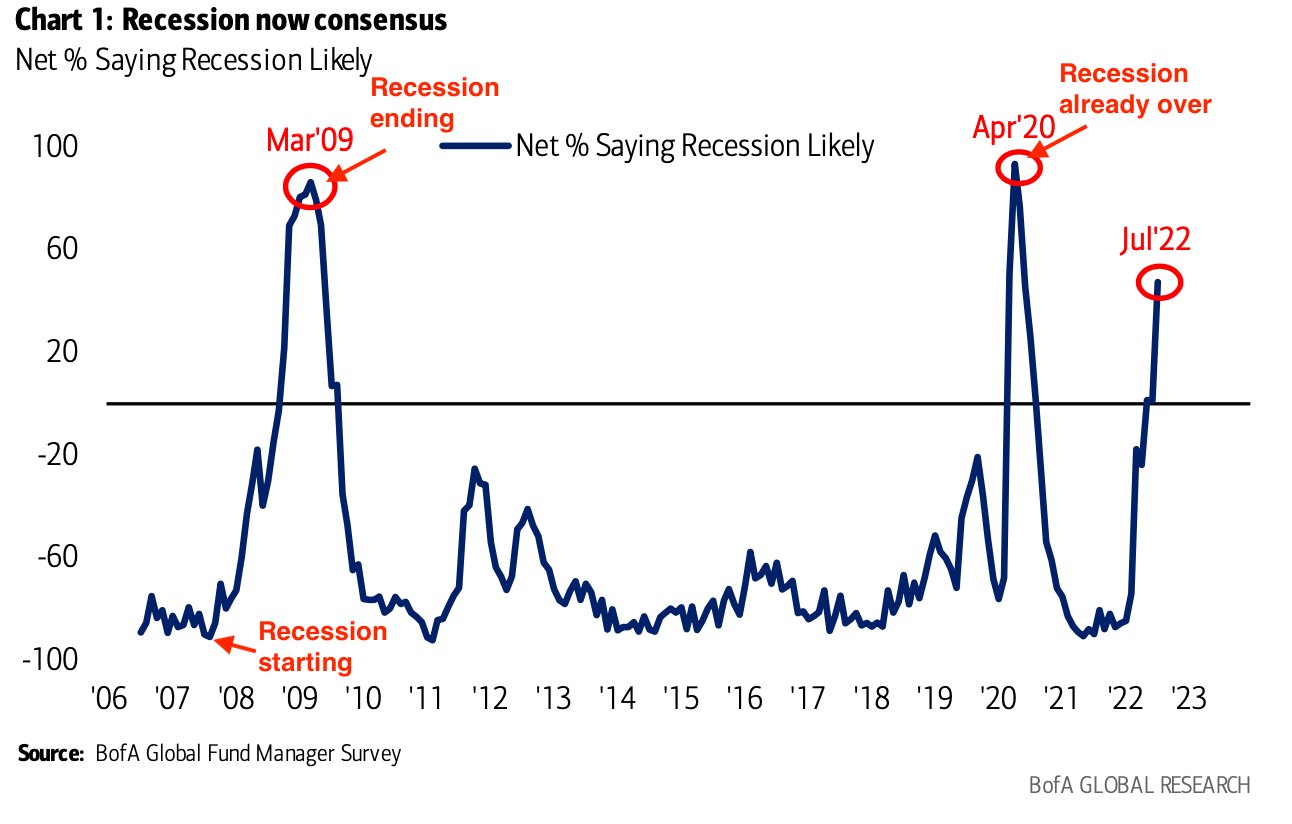

Looks like everyone and their mother now believes we are either in a recession or headed for one. Like I’ve said, I don’t care whether a slowdown gets labeled “recession” or not. Makes no difference one way or the other.

But here’s an interesting chart from BofA’s research group:

Admittedly, there aren’t a lot of recessionary data points here, but the gist is that when the percentage of fund managers that answer “yes” to the question of “whether or not we’re in a recession” exceeds the nays by a wide margin, we tend to be moving closer to brighter days.

That said, the blue line could rise higher, but remember who’s being surveyed here. These are fund managers, and they love to talk their own books. If so, this would indicate that a lot of money managers are defensively positioned or heading that way.

And if that’s the case, what do you think has happened to the multiples in those low-growth sectors and stocks?

Remind them why they pay you

If you think your book is down, BlackRock announced that they lost $1.7 trillion in clients’ money in the first half of the year. Wow!

I guess it makes sense. A moderate portfolio passively invested in 60% SPY and 40% AGG lost almost 17%, and BlackRock was at $10 trillion at the end of 2021. Since passive ETFs are something like 80% of BlackRock’s business, being down $1.7 trillion is about right.

We talk a lot about why most absolute numbers are meaningless in this business. Relative ones are more important, but I must say that seeing a number like $1.7 trillion leaves a mark.

I’d wager that a lot of advisory clients would see a story like this, look at their own portfolios, and conclude that there’s no reason to pay an advisory fee when they could just be passive and get the same gross return.

And you know what? I agree! If they’re only looking for performance, could care less about things like cash flow planning and income, and can comply with a true passive strategy (aka don’t panic and never deviate), then go for it.

My very unscientific opinion assumes that about 3% of investors are suited for passive management. The rest need help because they are emotional basket cases, risk running out of cash in retirement, etc.

I know I’m preaching to the choir here, but clients must understand that the asset management stuff is a component of the overall value you bring to them.

Shrinkflation sucks

We recorded a podcast a few weeks ago on inflation and all the other “flations” out there, like greedflation. By far, the most frustrating is shrinkflation. That’s when companies don’t raise their prices but rather shrink the size of their product or service.

I first noticed this concept take hold in NYC back in 2016. Before then, when I ordered a martini at any respectable establishment on the island, that martini was filled to where the meniscus touched the top edge of the glass in a way where even the smallest additional drop of liquid would cause it to spill.

Furthermore, there was an unwritten rule that if you ordered three martinis, the fourth was on the house. Didn’t matter where you went either. It was code in NYC.

But starting in 2016, everything changed. They began serving martinis in thimbles, and this trend has since spread across the country to the point where I’ve stopped ordering drinks when I go out. Not that I want to stumble home from lunch to two small kids. Far from that. I just hate spending $20 for something that is legit half the size of where it was like 4 years ago.

And then I read this week that restaurants in NYC are now serving 4oz wine pours. Oh, man, am I glad I don’t live there anymore. I’d burn the city down.

But the bigger question I have for those who still live there is why hasn’t anyone else burned it down? What New Yorker would ever tolerate such abuse? When I lived there, the only way to survive was to stand ready to shred anyone at any time over anything. That’s what made it so special.

Has NYC become yet another “thank you, may I have another” enclave for participation trophy winners who found someone else to pay their rent? That’s too depressing to even imagine.

Try to enjoy the weekend. If it’s even possible after contemplating such a question.

You must be logged in to post a comment.