Happy Friday!

This week, I wrote about five reasons why the current “crisis” isn’t like the last one. Not trying to beat a dead horse, but clients need to realize that today is a story about bonehead decisions by a handful of executives at banks (as always, reach out if you’d like a copy).

The GFC was a complete dismantling of the foundational trust that makes finance work due to pervasive risk-taking, one clinically insane accounting rule, and leverage.

Here’s the TLDR version: Today = idiosyncratic, 2008 = systemic

Moving on…

Catching up

Here’s a brief summary for those who haven’t been paying attention and want to get caught up on what’s transpired over the last two weeks.

And click here for a TLDR on how the dumpster fire that is Debit Suisse was finally put out (along with some swag below).

The fact that CoCo bonds are in the news is all the evidence needed to prove that the media is running out of fuel for this current crisis. These aren’t even issued outside of Europe, and the exposure to these from U.S. institutions appears to be minimal.

But if you’re wondering why anyone would ever own them, simply revert to the famous quote below from Raymond DeVoe:

“More money has been lost reaching for yield than at the point of a gun.”

Lastly, if you’re also wondering how SVB could have flat-footed so many smart VCs and Silicon Valley’s Hoodie Nation, here’s a quote from Jeremy Grantham that perfectly summarizes how the broader financial services industry operates:

“The central truth of the investment business is that investment behavior is driven by career risk. In the professional investment business we are all agents, managing other peoples’ money. The prime directive, as Keynes knew so well, is first and last to keep your job. To do this, he explained that you must never, ever be wrong on your own. To prevent this calamity, professional investors pay ruthless attention to what other investors in general are doing. The great majority ‘go with the flow,’ either completely or partially. This creates herding, or momentum, which drives prices far above or far below fair price. There are many other inefficiencies in market pricing, but this is by far the largest.”

So, yes, we should have known.

There’s a lot of “how could this have happened” talk right now. As in, we all should have known this was coming because most of what was needed to assess this situation existed in the footnotes of Silicon Valley Bank’s financial statements.

Barry Ritholtz rightly points out that we’re likely not to know the whole story until some famous financial writer publishes a book, but I’ll take a SWAG at it.

Perhaps the bank run seed was planted when influential tech writer, Byrne Hobart, tweeted back in February that SVB was insolvent and levered 185:1.

Then there’s Moody’s. They have a pretty good track record of causing financial crises, and Moody’s was about to downgrade SVB. Maybe that leaked before SVB called Goldman to fix their problems.

And now we’re learning that the San Francisco Fed had appointed a team of senior examiners over a year ago to assess SVB. Not at all surprised because name one time in history that a regulator ever stepped in before something bad happened. Just one.

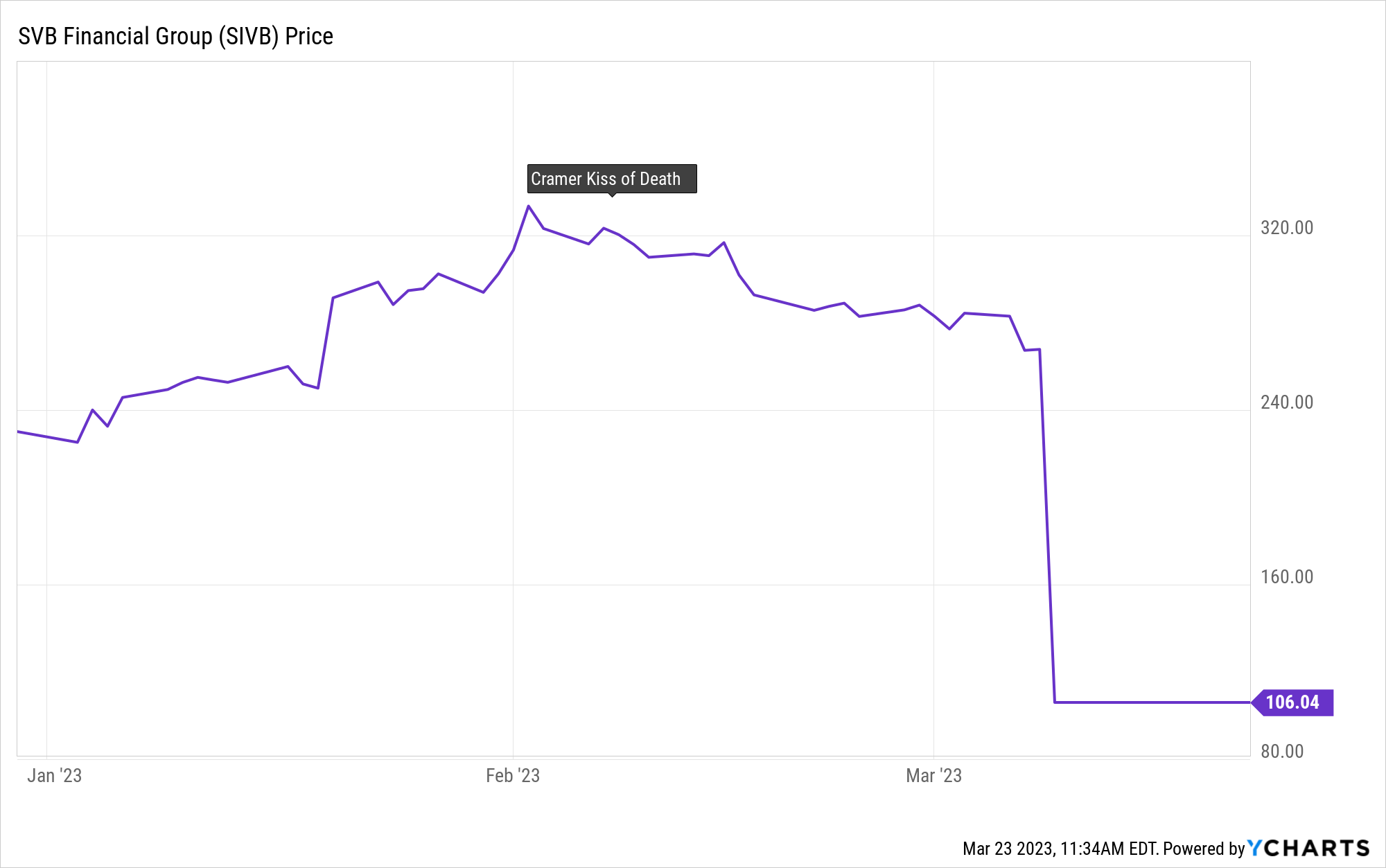

But arguably, the biggest red flag came from Jim Cramer. Weeks before SVB collapsed, he gave the stock a clean bill of health on his show with all those loud horns and sound bites.

Right then and there, the world should have known. No stock can survive the Cramer Kiss of Death.

Speaking of Cramer…

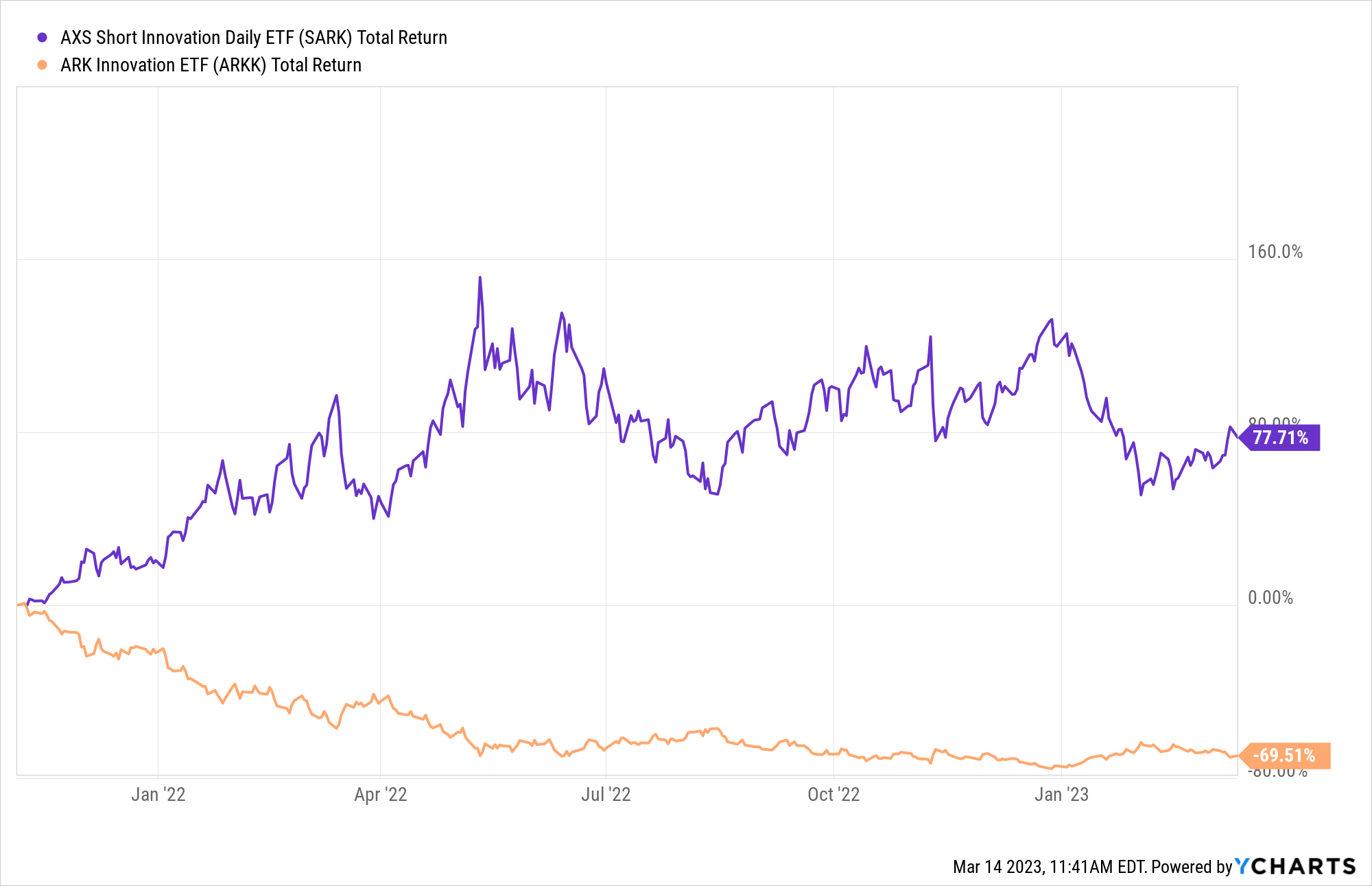

After months of anticipation, SJIM is finally up and running. Yes, this is the newest ETF from Tuttle Capital Management that shorts all the stocks Jim Cramer recommends on television or online.

Tuttle is the same firm that brought us the short Cathie Wood ETF that’s done “just ok” since inception through mid-March:

I’ve read maybe three ETF prospectuses (prospecti?) in my life, but I had to make this my fourth for what I assume to be obvious reasons. Mostly, I had to know how this ETF works.

And it didn’t disappoint. The strategy requires three Tuttle employees to watch Cramer on television all day, monitor his Twitter account, etc. That’s probably why the fund charges 1.2% (think about the internal cost to continually medicate those poor souls).

To be clear, that’s not a dig on Cramer, per se, but rather an admonition of the current state of financial news and social media. I’d rather watch C-SPAN all day. Sober.

In fact, I sort of feel bad for Cramer and Cathie Wood. This is a savage dig at two highly successful people that I must assume never drew first blood against Tuttle.

It seems like Ms. Wood has been professional about it, but if I were Cramer, the gloves would come off. I’d go on my prime-time television show to tell the world to go long SJIM.

That’s right. I’d hit every horn and do that “BUY BUY BUY” like 30 times in a row. Just to be sure all three Tuttle researchers couldn’t miss the recommendation during a bathroom and/or Xanax break.

Think about it. The fund has to then short itself, right? If their investment mandate is to do the inverse of Cramer’s recommendation, the fund would violate its raison d’être if it didn’t.

But can a fund short itself? I really don’t know, and even trying to think it through leaves me more confused than trying to solve the grandfather paradox.

Enjoy the weekend…

You must be logged in to post a comment.