Happy Friday!

I get asked a lot by investors if we’re ever short the market or a particular stock. There seems to be a conceptual understanding of short selling but also a misconception of the mechanics and risks involved.

Hence, I wrote a primer on short selling and why it’s best left to hedge funds and ETFs targeting professional investors. Reach out if you’d like a copy.

Moving on…

Conflicting signs.

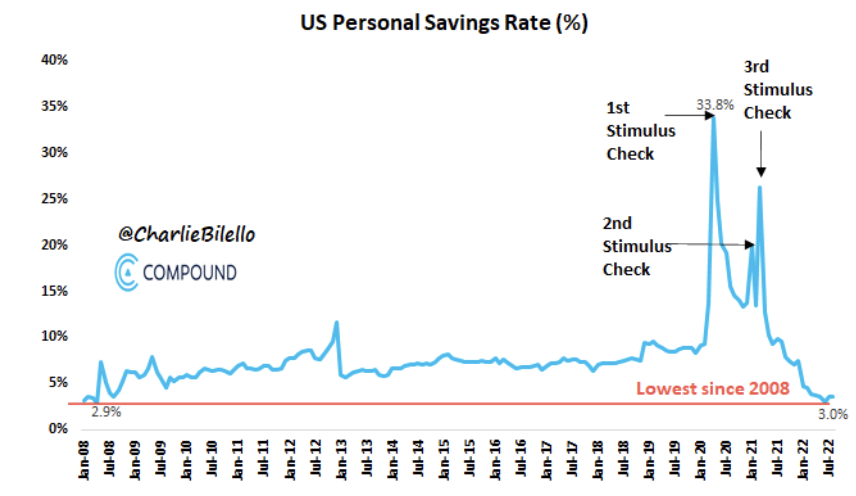

Third quarter GDP came in positive and so much that I don’t see how the “we’re in a recession” debate has any legs. More specifically, consumer spending is holding up. How is this happening with inflation so high?

First, the job market is still strong. Yes, it’s showing signs of softening, but there are still 1.6 jobs for every person looking.

Second, per Charlie Bilello’s excellent blog, consumers are saving less (lowest savings rate since 2008) and borrowing more (highest increase in consumer credit since 2011).

Third, home equity is at levels unseen since the 1980s. Assuming banks continue to offer HELOCs and consumers tap them, more dry powder could come.

To be clear, I’m not saying these are good trends but rather why consumer spending remains somewhat robust.

On the flip side, the yield on the 3-month Treasury exceeded the 10-year on Wednesday, and that’s something we can’t ignore. Yield curve inversions have been discussed extensively here, but most of the focus was on the 2yr-10yr inversion because that happened earlier this year.

The concept is the same with the 3-month, but since this is shorter than the 2-year, some think it’s more predictive. Add a very mixed earnings season on top, and it’s just a strange economic environment.

So far, my view remains unchanged. The economy is slowing down, but it’s not a recession yet. Mid-to-late next year is likely a different story.

It’s official!

Since Elon Musk announced his intent to buy Twitter, I’ve said little for fear of jinxing the deal. If this were to fall through, I don’t know if I could stomach the disappointment.

But as of today, it’s a done deal, and he’s already started cleaning house. Couple points.

First, the appetite for owning this debt is a lot different than six months ago. Banks are a lot like car rental companies. They like to make loans just as car rental companies like to make reservations, but neither want to keep them.

So, most banks, in most deals, will go out to their large investor clients and offer to sell them these bonds even before the deal closes. Then, once the deal is consummated, the debt is immediately sold off in pieces to those large investors.

It’s seen as a win-win. The bank earns an upfront spread on selling the bonds to investors and inoculates itself from the risks of owning bonds (interest rates, inflation, and default). Large investors get assets they can try to profit from over time (coupons and trading).

There’s another reason why banks don’t want to keep this debt. Thanks to the GFC, banks are required to maintain strict capital ratios. If they do risky stuff, they have to pay the price.

Let’s say a bank doesn’t sell off these bonds and keeps them because they pay strong coupons or whatever. For every dollar of debt they own, a percentage of their total assets has to be held in the vault at the Fed.

So, if the bank wants to hold $1 billion in debt over 30 years, it may need to take $20 million of its existing capital base (making that number up) and give it to the Fed for safekeeping.

This implies that owning bonds is not only risky for a bank but also expensive because there’s an opportunity cost (that $20 million could have been loaned out, etc.).

The Twitter saga is interesting because six months ago, the demand for debt from this deal was so high that Elon got something like $13 billion in commitments from a consortium of banks. But today, that demand has dried up.

Perhaps it’s the most hawkish Fed in 40 years, or it could be that Elon’s public bashing of the company over the last six months spooked would-be debtholders. Whatever it is, banks have two options:

- Sell the debt at a significant discount and get their faces ripped off.

- Hold the debt, wait for the market to improve, and then slowly sell it off to unsuspecting retail clients in their wealth management division (Liar’s Poker 2.0).

Well, it appears they are going with option #2.

Second, and if you’ve been reading this fledgling blog for some time, you’ll know where I’m headed; the memes are the icing on the cake. There have been some stellar ones so far, like here, here, and here:

But my gut tells me this is just the beginning. Giddy up.

Masterpiece on crypto

Matt Levine is the best financial writer out there, and he wrote a cover-to-cover issue for Bloomberg Businessweek about cryptocurrencies. I’m halfway through, and it’s stellar.

I’m serious. Anyone who wants to learn about cryptocurrencies, take the time to read this report. Levine’s ability to explain even the most technical aspects is unmatched.

But that’s not the masterpiece on crypto I’m referencing. Oh no, I’ve got something so much better than an educational piece on an asset class that grew to a peak of $3 trillion 10 months ago and now trades around $1 trillion.

Apparently, there is a famous bitcoin astrologer with 1.8 million social media followers. I’ll pause here to let that last sentence marinate for a moment. Seriously. Let every syllable attach itself to your soul, one at a time.

Stay with me because it’s about to get really, really good.

Her name is Maren Altman, and as you may have concluded, she offers investing predictions based partly on astrological interpretations. A newly surfaced court document shows she received $30,000 in marketing payments from the crypto lender Celsius Network in the months before it declared bankruptcy.

She is now being accused of taking the money in exchange for creating favorable content about Celsius (like the ad below) when it was tanking.

To be abundantly clear, the controversy and challenge to her credibility did not culminate from using patterns of stars to direct post-tax dollars from her Instagram followers. That was not only kosher but clearly a desired service.

She’s in hot water because she got caught promoting digital iron pyrite for profit. She sold out, and now all of her prior astrological predictions come into question. Couple of points here.

First, the laughable insanity of this story sheds light on just how screwed Celsius must have been when all this went down. It’s one thing to steal $17 million days before freezing client accounts, but to hire a crypto astrologer as a last-ditch effort to save the company is next-level desperation.

Second, should we feel bad for all these Gen Z-ers that can no longer find a trusted source for astrological investment advice? Or should we dread the onslaught of TikTok pity parties that are almost certainly invading the internet as we speak?

Enjoy the weekend…

You must be logged in to post a comment.